Priors № 1 — The Pattern That Wasn't

Why most patterns in markets are noise in costume — and the test that tells them apart.

Give a person enough market data and they will find a pattern. This isn't a flaw in any particular person; it's what minds are for. We are pattern-finding machines, tuned to spot the predator in the grass — and just as tuned, in markets, to invent one.

Markets are unusually cruel about this, because they are mostly noise, and noise is a gifted impersonator. Flip a coin two hundred times and you'll see streaks, momentum, and clean reversals that look exactly like skill. Plot them and a confident story writes itself. The story will be wrong, and it will feel true.

So the first job of a systematic investor isn't to find patterns. It's to distrust them.

We ran the experiment

We didn't want to assert this; we wanted to show it. So we ran a small experiment you can run yourself — the code is a single file of standard-library Python, no libraries required.

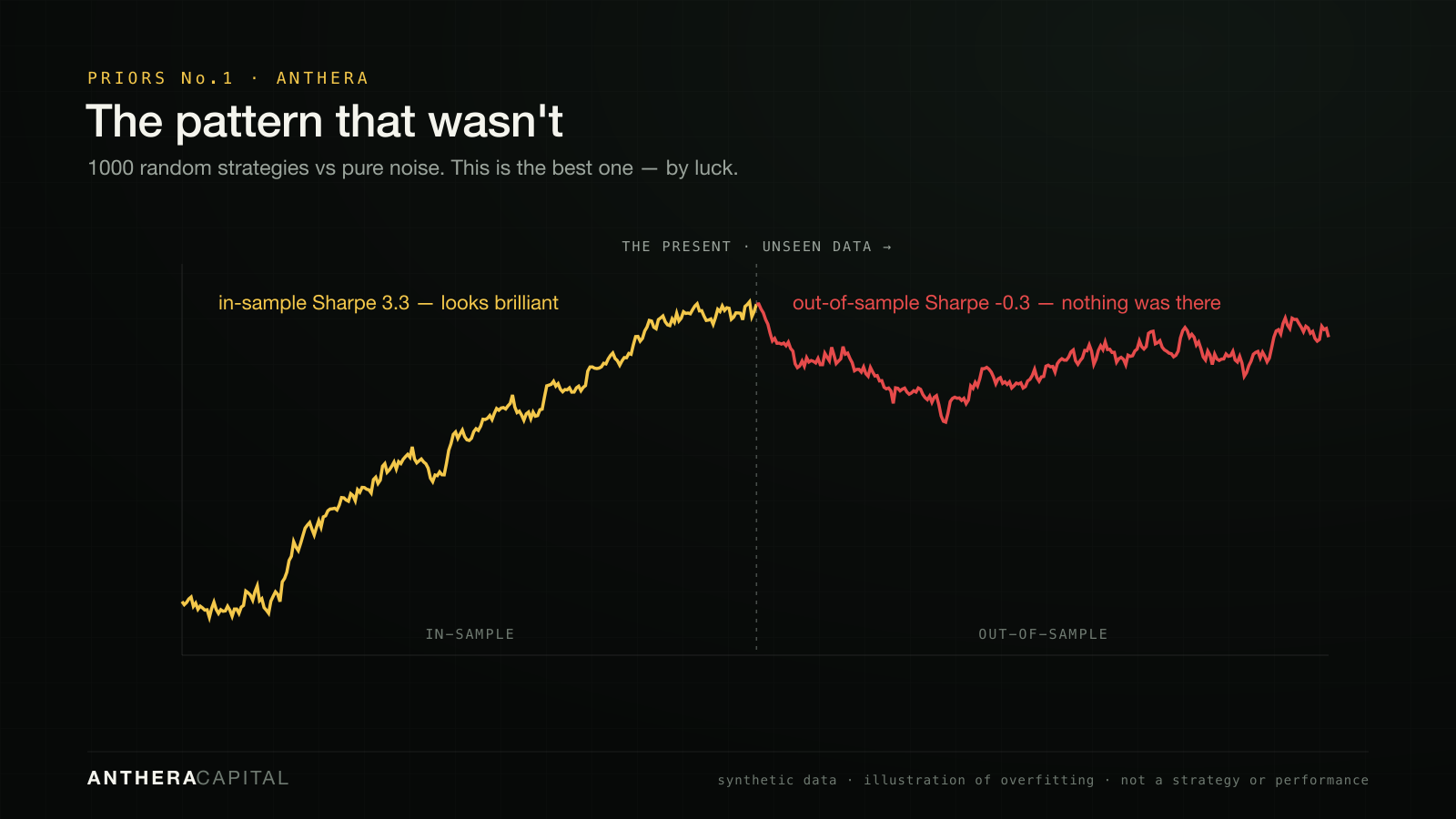

Take a market that is pure noise — zero expected return, nothing real to find. Invent one thousand random "strategies," each just a sequence of coin-flip long/short bets. Test them all on the first year of data, and keep the single best one.

That winner posted an in-sample Sharpe of 3.3 — the kind of number that makes you want to bet the book. On data it had never seen: −0.3. Nothing was there. We just searched until noise looked like genius.

The technical name is overfitting, sharpened by the multiple-comparisons problem: test enough ideas and one will look brilliant by luck alone. A strategy bent to fit the past will swear it can predict the future.

The test that matters — and the catch nobody mentions

The obvious fix is to check whether a pattern survives data it has never seen. That's right, but it's where most people stop, and stopping there is its own trap.

Out-of-sample isn't a test you run. It's a budget you spend. You only get truly unseen data once — the moment you look at it, tweak the strategy, and look again, you've quietly turned your test set into your training set. So the discipline isn't running the check; it's rationing it, and being honest about every strategy you tried and discarded along the way.

Which means the real number was never the in-sample Sharpe. It's the in-sample Sharpe penalized for how many times you went looking. A 3.3 from one honest attempt and a 3.3 picked from a thousand are not the same number — only one of them is real, and it usually isn't the one in the pitch deck.

So before a signal earns the right to move a single dollar, we hold it to three conditions:

- Measurable — defined precisely enough that two people compute it identically, with no room left for hope.

- Repeatable — present across time, instruments, and regimes; not a one-off coincidence dressed as a law.

- Out-of-sample — it survives data that played no part in building it, and we account for how many shots we took to find it.

A signal that clears all three still isn't guaranteed; markets change and every edge decays. But a signal that fails any one of them isn't an edge — it's a story you got lucky with, and stories are expensive when you size them like truths.

Why this is the whole game

This sounds like caution, and it is. But caution here isn't timidity — it's how capital is protected from the most common way sophisticated people lose money: believing their own backtest.

The discipline of distrusting patterns is unglamorous. It throws away most of what looks promising and says "we don't know" far more often than "we found something." But it's the difference between a system and a gambler with good vocabulary — and over enough decisions, that difference is everything.

We'd rather act on a few things we can defend than many things that merely worked once. In live markets, what you refuse to believe is as important as what you act on.

That's the first of our priors: the pattern you can see is guilty until proven innocent.

The experiment above uses synthetic data to illustrate a statistical trap. It is not a strategy, a backtest of any real approach, or a representation of any performance. For informational purposes only — not investment advice. Anthera is pre-launch and not currently raising capital.