The Operating Loop

Why the move you can clearly see is usually the move you already missed — and the framework we built for the ones you can't.

Markets do not wait. By the time a pattern is obvious enough to act on with confidence, the market has usually already acted on it. The move you can clearly see is, more often than not, the move you already missed.

This is the central, uncomfortable fact of live markets: the information that feels safe is old, and the information that is valuable is uncertain. Most investing is built to manage that discomfort. We build to work inside it.

Here is how we think.

What an unaided operator is positioned to lose

A talented investor can do remarkable things. But in live markets they are fighting two battles they cannot win — and one they usually don't notice.

The first is breadth. We don't mean speed in the way a market maker with a microwave tower is fast; that is a different sport, and not ours. We mean watching more instruments, more venues, more conditions, continuously — and applying the identical rule on the four-hundredth decision as on the first. A person can be brilliant and still be inconsistent. Inconsistency is the leak.

The second is emotion — and it deserves more than a line, so we'll give it its own piece.

The third, the quiet one, is hindsight wearing the costume of risk management. Most risk tools tell you what already happened. They are precise, well-formatted, and late. By the time the number turns red, it is no longer risk — it is a loss with a timestamp.

None of these are failures of intelligence. They are failures of architecture. A person is the wrong instrument for a job that rewards reading everything at once, feeling nothing, and noticing trouble while it is still ambiguous.

What we are, and what we are not

The answer is not a smarter human. It is a different instrument.

We should be precise, because the field is loud with people promising the impossible. We are not building something that predicts prices — we think prediction is the wrong goal, and we'll come back to why. What we are building is narrower and, we think, more honest: a system designed to read live markets faster than emotion can react, and to act only when its conditions are met.

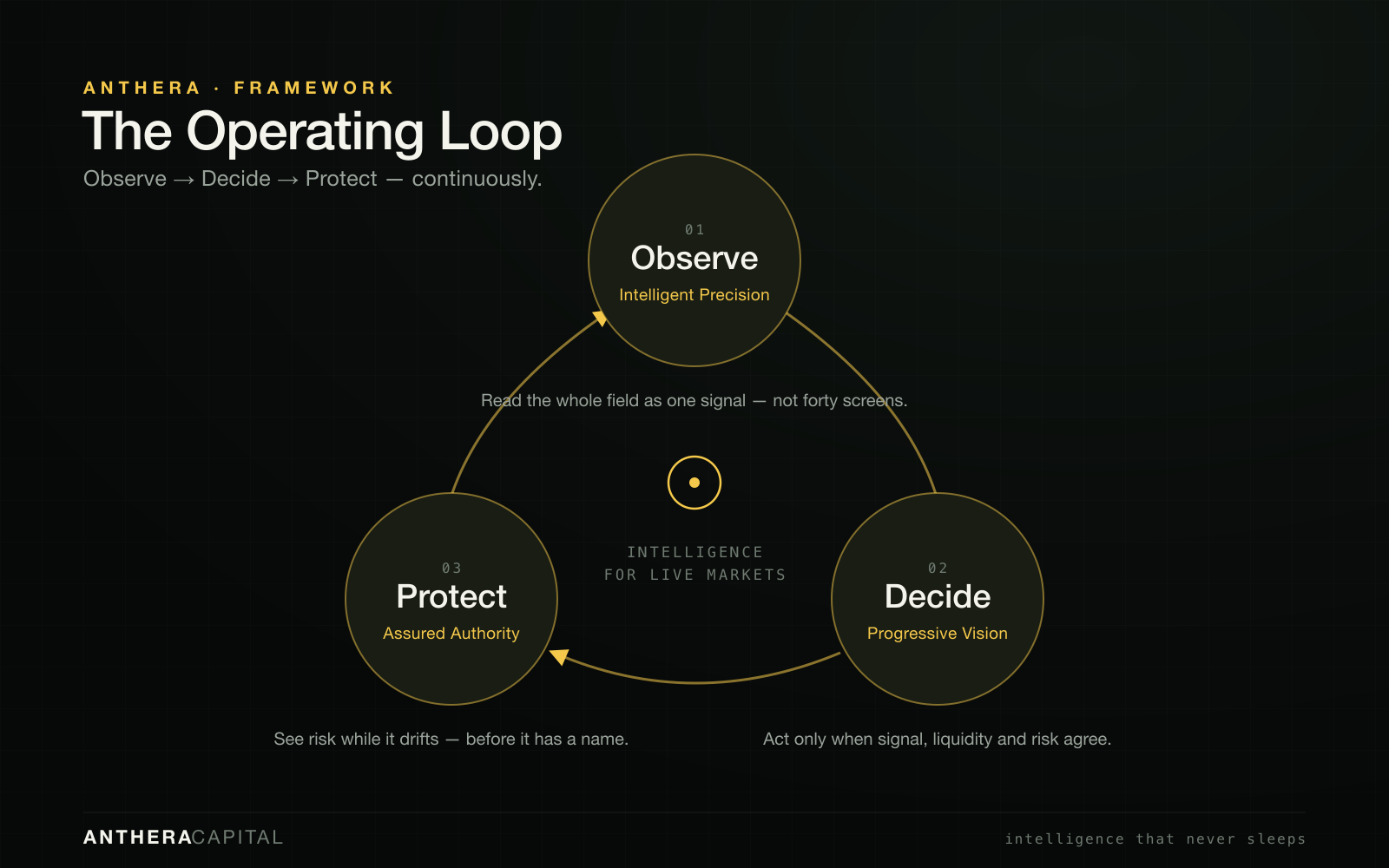

We call the shape of it the Operating Loop.

Most investment operations are three disconnected systems pretending to be one: something watches, something trades, something tallies the damage after. The money leaks in the gaps between them — between seeing and deciding, and between deciding and managing the risk. We build them as one loop. Three movements, continuously.

Observe. Live quotes, depth, and recent history, normalized into one comparable field — so that pressure building on one venue, depth thinning on another, and volatility shifting underneath both are read together, not on forty separate screens. The work here isn't collecting data; everyone has data. Here's a view we'll defend: the price everyone quotes is often the least informative number on the screen. The signal is usually in the disagreement around it — which venue is paying up, where the book is thinning, how far bid and offer have drifted apart — because that disagreement tends to move before the price does.

Decide. This is where most "systematic" descriptions go vague, so we won't. A pattern is permission to look closer, not permission to act. And the real question is never "is the signal there" — it is what is this signal worth, net of what it costs to express right now. A strong signal into thin liquidity isn't a green light; it's a sizing problem. Signal, liquidity, and risk aren't three gates that happen to line up — they're one calculation, and most of the work lives in the trade-off between them, not in the signal alone.

Protect. We can't see the move coming; anyone who says they can is selling something. What a system can do is refuse to look away. Exposure, liquidity, and volatility are watched continuously, so that when the conditions that have historically preceded trouble begin to line up, the position is already being trimmed — not because we predicted a drawdown, but because we stopped pretending a position that still looks fine on paper is the same as one that's still safe. And those risk conditions earn their place the same way any signal does: they have to survive data they've never seen, or they don't get a vote.

Then the loop closes and begins again — the same question, asked continuously: given everything visible right now, what is the disciplined thing to do, and is doing nothing the better answer?

A view we'll defend

If we hold one belief that isn't consensus, it's this: most edges don't stop working because the world changed. They stop working because everyone else found them. An edge is a crowd that hasn't arrived yet. So we care less about how good a signal looks on past data and more about its capacity and obscurity — how much can be done with it before the crowd arrives, and how long that takes. A beautiful backtest on a crowded trade is just a well-documented way to be late.

It's also why we trust the graveyard more than the trophy. We once took a thousand random strategies — pure coin-flips — and ran them against pure noise; the best one looked brilliant on the data we picked it from and was worth nothing on data it had never seen. The strategies you reject, and your honesty about how many you tried, teach you more about what's real than the one that survived.

The traits, and what backs them

Three traits hold the loop up. Don't take the names on faith; each is only as good as the constraint behind it.

Intelligent Precision constrains what we observe: a signal counts only when it is measurable, repeatable, and survives data it has never seen. Everything else is a story someone got lucky with.

Progressive Vision constrains how we decide: read conditions while they're still ambiguous and act on probabilities, not certainties — earlier, smaller, and more reversibly than instinct would.

Assured Authority constrains how we manage risk: it sounds like confidence; in practice it's restraint. The hardest thing a disciplined system does is not act — stay flat when the signal is weak, the book is thin, or the risk doesn't justify the move. Most of the damage in any portfolio is done by trades that should never have happened.

The standard

This is a high bar, and we hold it as one. A system worth trusting isn't built by being clever once. It's built by being disciplined continuously — in the research that admits when a signal is just noise, in the engineering that makes the loop fast and legible, and in the restraint to do nothing when nothing is the right answer.

We'll write here about how we think: signal and noise, risk and regime, what models can and can't capture, and the strange discipline of letting a system decide. We won't tell you what we're trading, and we won't tell you what to buy. The edge is in the method. The method is what we'll show.

Anthera Capital is a systematic investment research and technology company. This is for informational purposes only — not investment advice, an offer or solicitation, or a prediction of any result. Anthera is pre-launch and not currently raising capital.